TL;DR

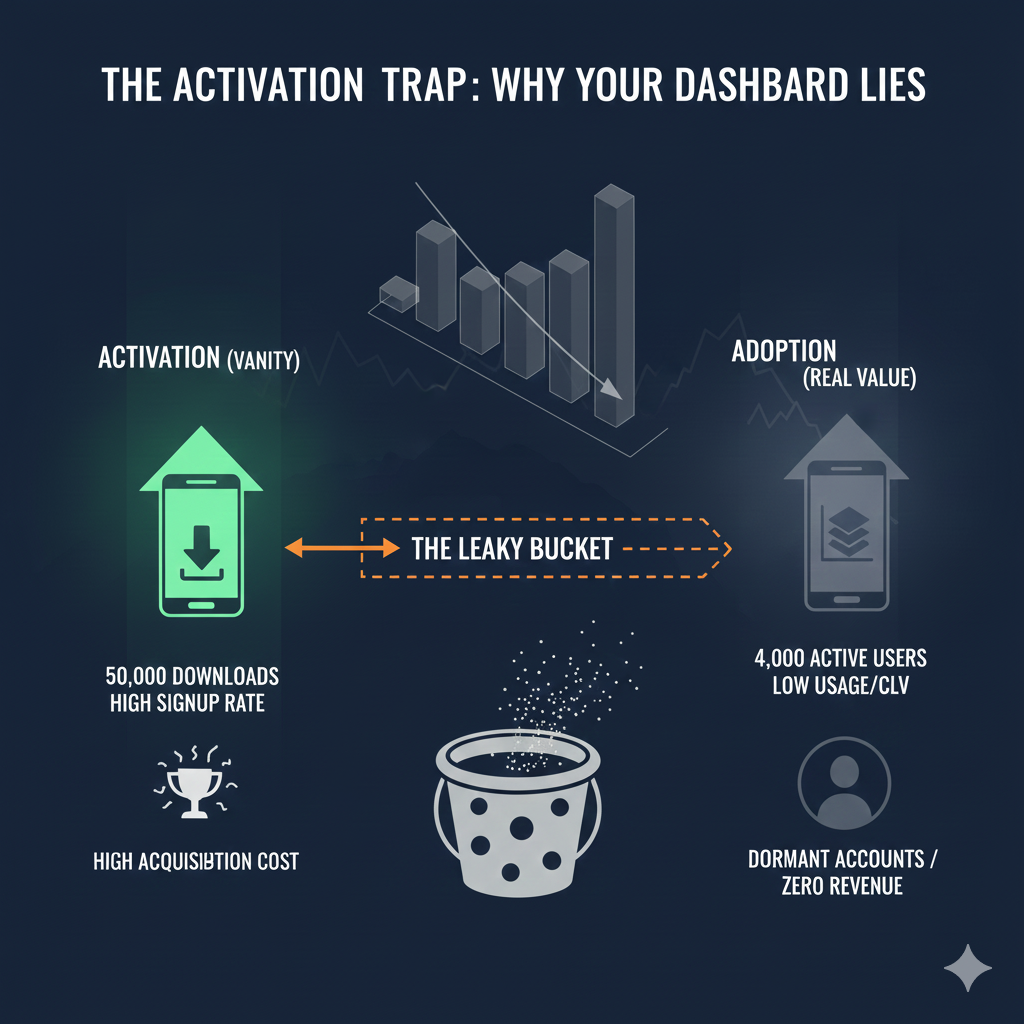

You launch a new mobile savings tool.

Marketing spends thousands on the campaign.

The dashboard shows 50,000 downloads in the first month.

Your "Activation Rate" is through the roof. Everyone celebrates.

Three months later, you look at the usage data.

Only 4,000 users have opened the tool more than once.

The rest? They downloaded it, logged in once, and never returned.

This is the Activation Trap.

You celebrated the signup, but you failed the habit.

Most CX leaders and digital banking heads measure success by the starting line (Activation) rather than the finish line (Adoption).

But in 2026, activation without adoption is a vanity metric.

It creates a "leaky bucket" where acquisition costs are high, but lifetime value (CLV) is stagnant.

This distinction between access and behavior is increasingly being called out by industry experts studying customer experience for retail banking. As McKinsey’s Global Banking Practice notes, “Digital adoption is not about access it is about behavior. Banks that win are those that design experiences customers return to, not just platforms they can log into.”

This insight highlights why traditional customer experience metrics fail to capture real value creation. A customer who can log in but does not return has technically “activated” yet from a customer experience perspective, the bank has failed to embed itself into the customer’s financial routine.

The bitter truth that you must face? A customer who activates but doesn't adopt is actually worse than a non-customer.

Why? Because you paid to acquire them, you paid to onboard them, and now you are paying to service a dormant account that generates zero revenue.

To fix this, we must first define the difference clearly.

The gap between these two metrics is where your revenue disappears.

Activation is a binary event. It happened, or it didn't.

Adoption is a behavioral state. It is continuous.

The "Adoption Gap" is that 40% drop-off between signup and usage.

This is where CX optimization in banking needs to focus.

The critical distinction between adoption and activation creates a fundamental business challenge: high adoption does not guarantee activation, and activation failure is invisible in traditional adoption metrics.

Example scenario:

· Adoption metric: 85% of customers have activated mobile banking (app download + account linkage)

· Reality: Only 62% of those adopted customers have completed even one transaction

· Gap: 23% of adopted accounts are inactive - representing sunk customer acquisition investment with no realized value

This adoption-activation gap is particularly acute in retail banking because:

1. Enrollment inertia: Banks often bundle products or auto-enroll customers during account opening, inflating adoption metrics without corresponding activation

2. Onboarding friction: The gap between "account opened" and "first transaction" is where customers experience maximum friction

3. Feature complexity: Modern banking platforms offer so many features that newly acquired customers become overwhelmed, leading to passive account holding without active usage

4. Low switching costs for partial engagement: A customer can hold an adopted account without activating, then quickly shift to a competitor when needed, providing no relationship lock-in

Capgemini's research reveals the strategic consequence of prioritizing adoption over activation and lifetime value:

· 37% of banking leaders name product adoption as their primary success metric

· Only 28% of banking leaders prioritize customer lifetime value

· Only 29% of banking leaders focus on retention as a key metric.

This 37% vs 28% gap (9 percentage points favoring adoption) represents a fundamental strategic misalignment. When institutions prioritize adoption-count over lifetime-value, they create incentive structures that reward acquisition volume over engagement depth.

Why do high-intent customers (those who have activated) fail to become high-value adopters?

It’s rarely due to the fact that they changed their minds.

It’s because they hit friction during the critical "Habit Formation Window" (usually the first 30-60 days).

Here are the silent killers of digital product adoption in banking:

A customer opens your new budgeting tool.

It says: "No data available. Please link an account."

They try to link an external account. It fails or asks for micro-deposits that take 2 days.

They close the app.

Result: Activation (Opened tool) $\rightarrow$ Churn.

PXI™ Fix: Detect the "Link Failure" signal immediately and trigger an in-app guide: "Having trouble linking? Try this manual entry option to see how it works instantly."

You have a powerful "Auto-Save" feature.

But it’s buried three menus deep under "Settings."

The customer activates the savings account but manually transfers money (high effort).

Eventually, they get tired and stop.

Result: Low engagement.

PXI™ Fix: Use journey analytics to see they are transferring manually. Trigger a nudge: "Tired of manual transfers? Turn on Auto-Save with one tap here."

A customer activates a new rewards credit card.

But they don't add it to their digital wallet (Apple Pay/Google Pay).

Without physical card usage, their transaction volume remains low.

Result: The card is "Active" but not "Top of Wallet."

PXI™ Fix: Identify the "Active Card / No Digital Wallet" Pod. Send a specific campaign: "Add to Apple Pay today and get 2x points on your first tap."

You cannot solve adoption problems with activation tools (like email blasts).

You need Predictive Experience Intelligence (PXI) to intervene based on behavior.

Here is the PXI™ playbook to improve product usage in banks:

Stop looking at aggregate data. Look for clusters of behavior.

Why is Pod B going back to the branch?

PXI analyzes the signals: Did their second mobile deposit fail? Did the app crash? Was the fund availability too slow?

If PXI™ sees a "Deposit Failure" signal, it flags the root cause: Technical Friction.

Don't send a generic newsletter. Send a context-aware fix.

By using customer engagement banking strategies that are reactive to behavior rather than time, you move users across the chasm.

Investing in digital adoption strategy in banking is not just about UX; it’s about P&L.

The Math:

If you improve adoption by just 10% in a cohort of 100,000 new users:

It is time to change your scorecard.

Stop reporting "New Accounts" as your primary success metric.

Start reporting "Active Habitual Users."

Activation is vanity. Adoption is the real metric that retail bankers should look at.

Don't let your investment die in the "Valley of Death."

Use CX optimization in banking tools to hold the customer's hand until the habit is formed.

Because in the end, the most profitable bank isn't the one with the most app downloads.

It’s the one with the most app users.

Do you know how many of your "Active" users are actually dormant? PXI can show you the gap instantly. Book a Strategy Session with our CX architects at NUMR to fix this adoption gap now! Discover exactly where your customers are stalling and how to turn "signups" into "revenue" with the Predictive Experience Intelligence (PXI™) framework.

There is no single metric that defines digital adoption completely, but one of the most important indicators is the DAU/MAU Ratio (Daily Active Users / Monthly Active Users). This metric measures product stickiness — how frequently users return and engage with a banking app or digital product.

A high DAU/MAU ratio indicates that customers are integrating the product into their daily financial behavior rather than using it occasionally.

However, leading banks and fintech companies track multiple adoption metrics together, including:

Modern CXM dashboards increasingly combine these metrics with behavioral analytics to help banks identify:

The goal is no longer just tracking usage. It is understanding why adoption succeeds or fails across customer journeys.

Improving product adoption for older banking customers requires reducing friction, simplifying navigation, and increasing confidence during digital interactions.

Many banks mistakenly assume older users resist technology. In reality, behavioral analytics often show that older demographics have high intent but encounter usability friction during critical journeys.

Common friction points include:

To improve adoption among older demographics, banks should focus on:

Design interfaces with:

Reducing cognitive load significantly improves completion rates.

Interactive guided tours work better than static tooltips or documentation because they:

This is especially effective during:

Modern CXM dashboards help banks analyze adoption behavior by demographic segment.

For example, banks can identify:

This allows teams to optimize journeys specifically for that customer segment rather than redesigning the entire platform.

Combining digital channels with human assistance improves trust and adoption:

The most effective banking adoption strategies reduce friction before frustration occurs.

One of the most effective strategies for increasing credit card adoption is focusing on the customer’s first 5 transactions.

Behavioral studies across banking and fintech consistently show that customers who actively use a new card within the first 14 days are significantly more likely to:

This early activation phase is critical because customer habits form quickly.

A strong credit card adoption strategy should focus on:

Banks should reduce delay between:

This can be improved through:

Many banks focus only on transaction volume. However, adoption depends more on repeated behavior.

Instead of:

Focus on:

This creates behavioral habit loops.

Real-time engagement improves adoption dramatically:

Modern CXM dashboards help banks identify:

This allows banks to intervene before disengagement happens.

Adoption often fails because customers encounter:

Fixing early friction has a direct impact on:

The key insight is simple:

Early usage behavior determines long-term adoption.

Yes — product experience has a massive impact on cross-sell success in banking.

Customers will not adopt high-value financial products if they struggle with basic banking experiences first.

For example:

is significantly less likely to:

This happens because trust in digital banking ecosystems is cumulative.

Cross-sell success depends on:

Poor adoption in foundational products creates friction throughout the entire customer lifecycle.

These issues reduce confidence and engagement.

Leading banks now use CXM dashboards and behavioral analytics to:

This allows banks to:

For example:

A customer actively using:

is far more likely to adopt:

Q: What is the most important metric for digital product adoption in banking?

A: DAU/MAU Ratio (Daily Active Users / Monthly Active Users) is critical. It measures stickiness. Also, track "Time to First Value" (how fast a user completes a key task after signup) and "Feature Depth" (how many distinct features a user engages with).

Q: How do we improve product usage in banks for older demographics?

A: Simplify the UI and use "guided tours" rather than tooltips. PXI data often shows that older demographics have high intent but hit friction on small UI elements (font size, button clarity). Addressing this friction specifically for that segment drives massive adoption.

Q: What is a good digital adoption strategy in banking for new credit cards?

A: Focus on the "First 5 Transactions." Data shows that if a user uses the card 5 times in the first 14 days, they are 90% likely to adopt it as top-of-wallet. Incentivize frequency, not just volume, during the first 2 weeks.

Q: Does banking product experience impact cross-sell?

A: Absolutely. A customer who struggles to use your checking app will never apply for your mortgage. Poor adoption in basic products kills the funnel for high-margin products. Fixing adoption is the first step in any cross-sell strategy.

.png)

.png)

.png)